Credit card for grocery shopping

Published:

One key principle for saving money is to cut costs in a category with a high share of expenditures.

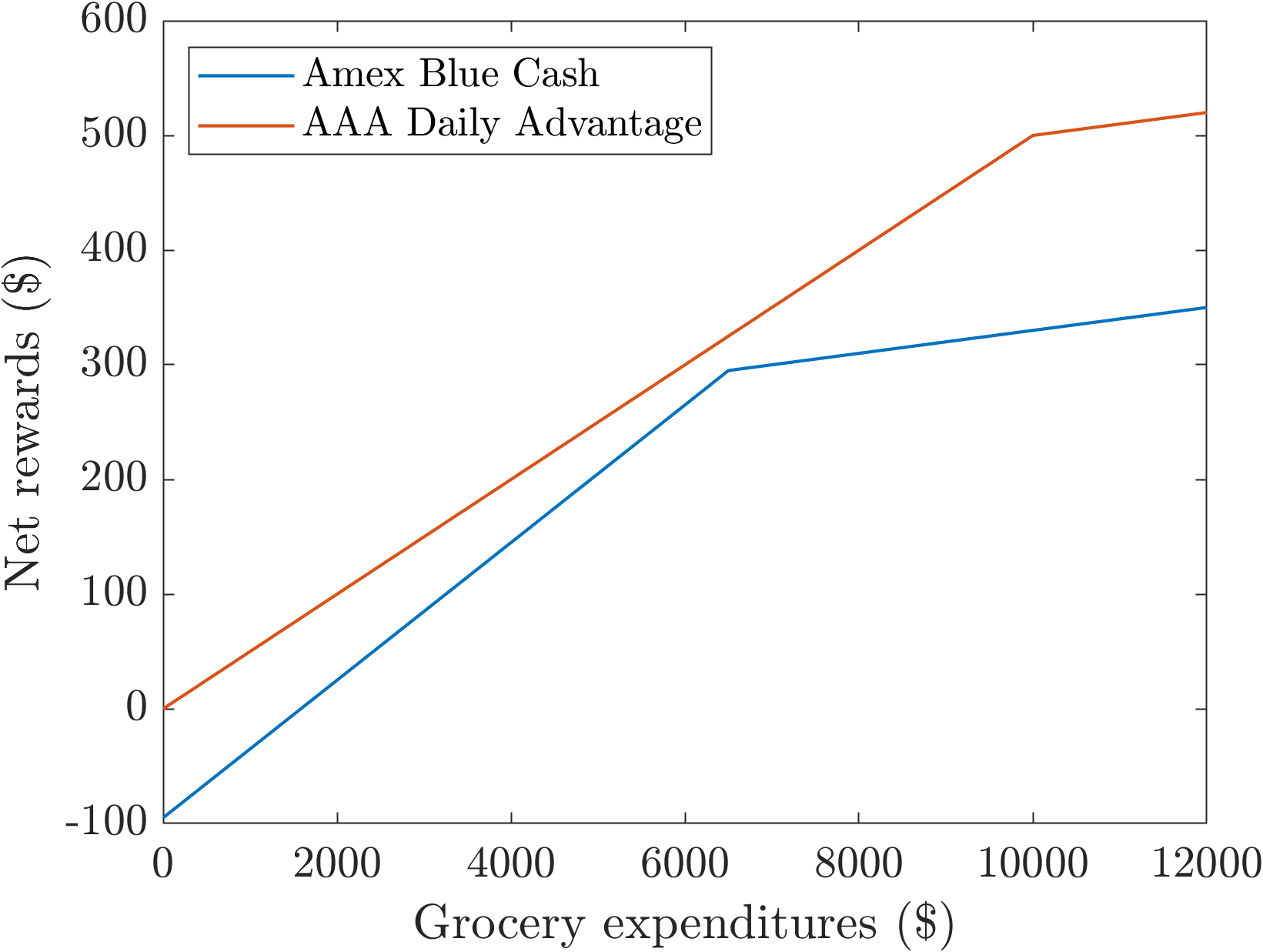

Grocery shopping is one of them for me. Since 2010, I have been using the American Express Blue Cash Preferred card, which I recently discussed in this post. Just to recap, the annual fee is $95, and the cashback rate on groceries is 6% up to $6,000 in purchases, after which it drops to 1%.

I asked Gemini for some good grocery shopping cards. Not surprisingly, the Amex Blue Cash Preferred card came on top, but there were a few others. One of them, the AAA Daily Advantage Visa Signature card, drew my attention. There is no annual fee, and the cashback rate on groceries is 5% up to $10,000 spent.

The AAA Daily Advantage card’s rewards surpass those of the Amex Blue Cash card (net of annual fee), as shown below. Let \(x\) represent grocery expenditure. Ignoring the accelerated earnings cap ($6,000 for Amex, $10,000 for AAA), the break-even point satisfies: \[\frac{6}{100}x-95=\frac{5}{100}x\iff x=9500.\] Since the break-even point is above the cap for Amex ($6,000) and the cashback rate of AAA weakly dominates Amex beyond $6,000, it follows that AAA always dominates Amex.

Does this mean I should ditch the Amex card? Not so fast. If we look at the benefit structure of the AAA card, there is also a 3% cashback on wholesale club spending, including Costco, but the accelerated cashback rate applies only to the first $10,000 spent. Recalling that the cashback rate on the Costco Anywhere Visa card is 2% (see here), and that my annual household expenditure on Costco is about $10,000, it is better to reserve the AAA card for Costco instead of other grocery spending. Of course, if my wife also opens an AAA card, then we can just use two AAA cards to cover our entire Costco and grocery spending without hitting the combined $20,000 cap. I will first experiment with the AAA card (which I applied for just yesterday) and see how it goes.