Toward Bubble Clarity

Published in Econ Journal Watch, 2025

In the fall of 2022, Tomohiro Hirano, Ryo Jinnai, and I studied a model in which the interaction between idiosyncratic investment risk, leverage, and the presence of a dividend-paying asset in fixed supply affects asset prices. This collaboration led to the working paper of Hirano, Jinnai, and Toda (2023) “Necessity of Rational Asset Price Bubbles in Two-Sector Growth Economies”, which we posted to arXiv in November 2022.

We submitted the paper to Econometrica in January 2023. It was rejected on May 5, 2023. One report was written by an expert and provided many comments. One of them was

Miao and Wang (2018, AER) … also study models of bubbles attached to assets with positive dividends/rents

and another was

I am not convinced by one of the main result of the paper that an equilibrium with rational asset price bubbles exists but equilibria with asset prices equal to fundamental values do not,

though this referee did not point out any specific mathematical error.

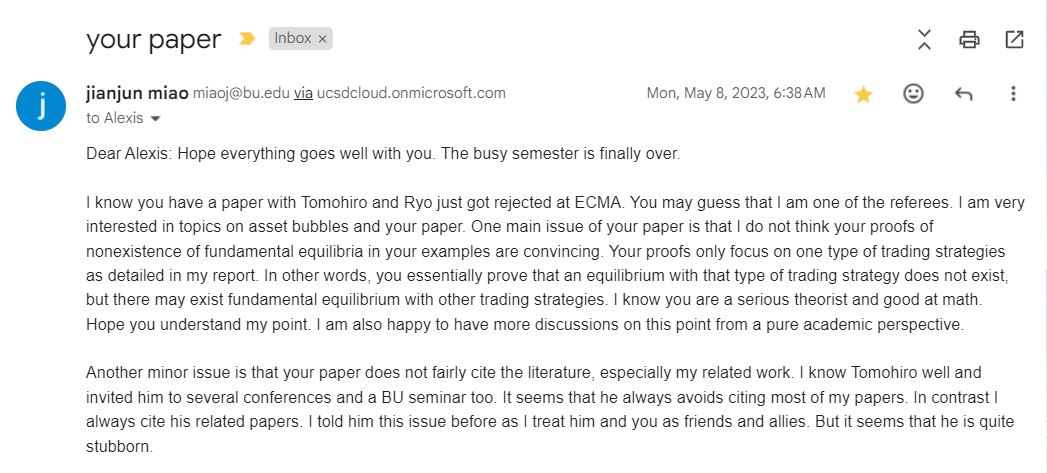

Three days later, on May 8, 2023, Jianjun Miao sent an email to me, in which he disclosed that he was the third referee at Econometrica.

In case it is difficult to read, I quote it here.

I know you have a paper with Tomohiro and Ryo just got rejected at ECMA. You may guess that I am one of the referees. I am very interested in topics on asset bubbles and your paper. One main issue of your paper is that I do not think your proofs of nonexistence of fundamental equilibria in your examples are convincing. Your proofs only focus on one type of trading strategies as detailed in my report. In other words, you essentially prove that an equilibrium with that type of trading strategy does not exist, but there may exist fundamental equilibrium with other trading strategies. I know you are a serious theorist and good at math. Hope you understand my point. I am also happy to have more discussions on this point from a pure academic perspective.

Another minor issue is that your paper does not fairly cite the literature, especially my related work. I know Tomohiro well and invited him to several conferences and a BU seminar too. It seems that he always avoids citing most of my papers. In contrast I always cite his related papers. I told him this issue before as I treat him and you as friends and allies. But it seems that he is quite stubborn.

The part “other trading strategies” is a bit strange, as our example employed a two-period overlapping generations model in which the unique portfolio choice in equilibrium is that the old sell the entire asset and the young buy the entire asset (which is necessarily true by market clearing). Anyway, we subsequently expanded this example as a new paper, which got published at Journal of Political Economy (after getting desk-rejected from Econometrica).

While working on the JPE paper, we learned about the Bubble Characterization Lemma of Montrucchio (2004), which states that a rational bubble exists if and only if the infinite sequence of dividend yields (dividend divided by the price) is summable. Using this result, it became obvious that the model in the 2018 AER paper of Miao and Wang does not generate rational bubbles (contrary to their claim in their abstract) because their model admits a steady state with positive dividends and prices. Thus, to clarify the confusion in the literature, when we published our 2024 JME review article, we wrote in Footnote 13 that the Miao-Wang model is different from the so-called rational bubble models.

Subsequently, we wrote several papers on asset price bubbles, and we received multiple (negative) anonymous referee reports claiming that we do not fairly cite the literature, that papers by Miao and Wang also study models of bubbles attached to assets with positive dividends, or that our research is just a derivative of the previous literature with a small twist. However, the Miao-Wang model is completely different from rational bubble models, so we felt the need to defend ourselves from biased referees and to clarify the confusion in the literature. This is why we wrote our paper initially titled “Rational Bubbles: A Clarification” and posted to arXiv in July 2024. After posting the working paper, we received supports from experts such as

I have in fact had doubts about Jianjun Miao’s claims that rational bubbles are easy to generate in production economies. Specifically, in one of his papers he conveniently omitted checking one of the key equilibrium conditions. I cannot remember now whether it was the 2018 paper or some other paper. It has always been surprising to me that they chose not to provide an explanation of how these models get away from Santos-Woodford powerful no-bubble theorem.

You have my full support. It is very important to find out when rational bubbles do exist, but not by contradicting the fundamental results.

and

We had a long discussion on Miao’s paper, we also had notes, but I could not find them anymore. I remember that paper was very confusing. In addition, we had noticed some misalignment between different uses of the concept of bubble, because there is some disagreement on the idea of fundamental, or intrinsic, value.

We submitted this paper to American Economic Review as a comment to Miao and Wang (2018). AER rejected our comment and sent us Miao and Wang’s referee report. (This report contains many false statements. You can read our response here.) There were other anonymous reports (who all recommended rejection), but only one of them seem to be written by an expert. Therefore, we decided to submit the paper to Econ Journal Watch.

After our paper went through peer review and got accepted at EJW, Miao wrote me an email:

Dear Alexis:

I just found that your comment paper Rational Bubbles: A Clarification is just published by Econ Journal Watch.

Your paper was rejected by all referees at AER. I think their reports are very similar and believe your comments on my AER paper with Pengfei do not make much sense. I do not understand you still insist on publishing it in some unknown journal that even does not ask us for a response. I do not understand what your point is. As both Pengfei and I have made it clear, we are in a small circle working on the area of bubbles. We treat you as a friend and ally. We should be friendly to each other to make this area more prosperous. We do not want to enter a bad equilibrium.

EJW always invites the commented-on authors to respond, so I am looking forward to Miao’s response. To us, what Miao, Wang, and the AER are doing are difficult to understand. If a model has been understood as a rational bubble model, but in fact it was not, it seems worth publishing a correction or a clarification. Instead, some editors and reviewers in the profession seem to try to silence us. In the above email, Miao wrote “We should be friendly to each other to make this area more prosperous. We do not want to enter a bad equilibrium.” Is he suggesting that we should rubber-stamp a paper of a “friend”? Is he suggesting that he will retaliate if we don’t do so, which is a “bad equilibrium”? We are not going to succumb to such intimidations. We are going to fight for truth and science.