Discretization

Published:

Discretizing probability distributions and stochastic processes

Published:

Discretizing probability distributions and stochastic processes

Published:

How this website was created

Published:

My personal thoughts on how to do research

Published:

Places that I have visited

Published:

How to string a racquet

Published:

Resources on LaTeX

Published:

Some tips for getting rich

Published:

List of my coauthors

Published:

Advices on applying to economics Ph.D. programs

Published:

Some tips for legally saving taxes

Published:

Published:

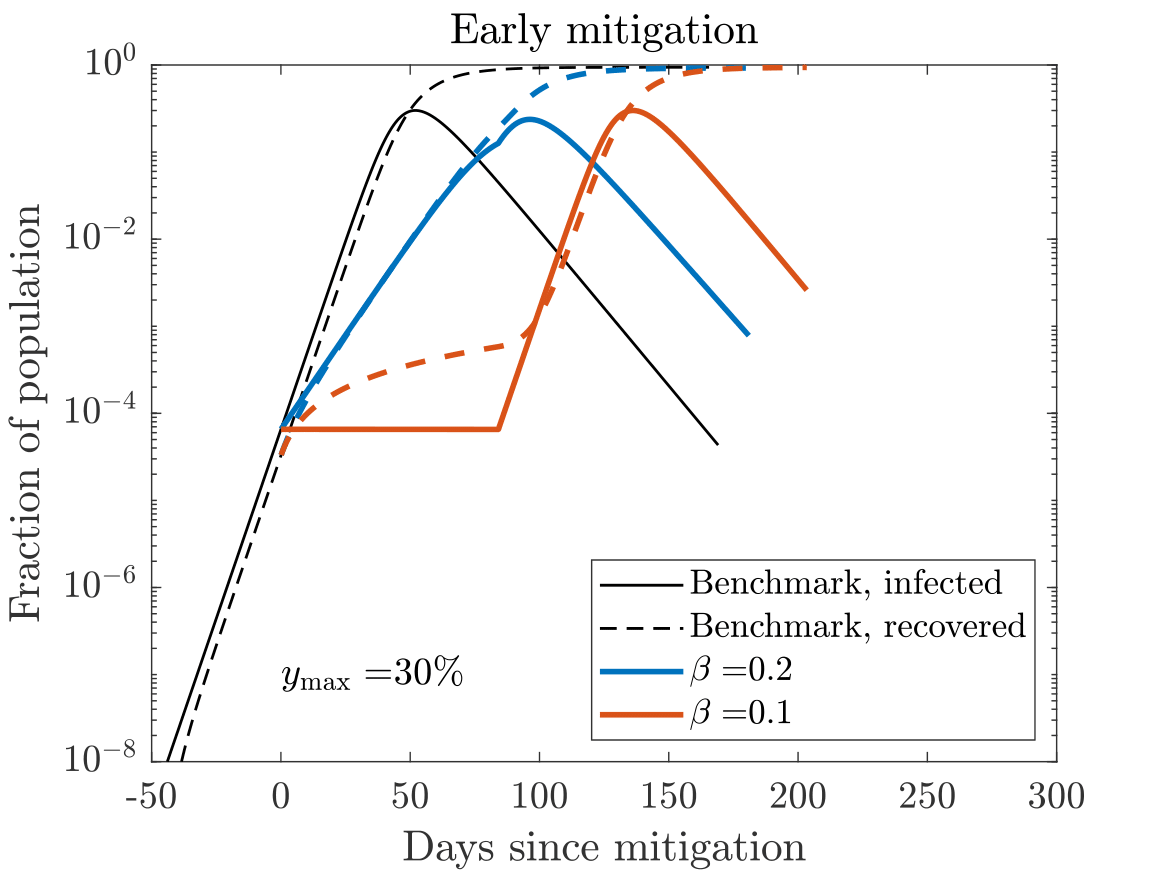

After returning from my UK trip in early March 2020, just a few days before the closure of the border, I got interested in COVID-19, like many of us. I played around with some models and I derived a system of differential equations that turned out to be identical to the Kermack & McKendrick (1927) susceptible-infected-recovered (SIR) model. I searched the literature and found the closed-form solution by Harko et al. (2014). At that time, little was known about COVID-19, so I decided to estimate the epidemiological parameters from data to predict the epidemic dynamics.

In mid March 2020, the state of California imposed lockdown, my kids’ school suddenly closed (teachers were not yet used to online teaching, so education was laissez faire to parents), tennis courts closed, and we could no longer eat at restaurants. I thought this was all wrong. I have a medical degree and knew about herd immunity, so just shutting down everything would simply delay the problem without solving it, while imposing significant economic costs to the society. So for the first time in my career as a researcher, I worked on a project not just driven by scientific curiosity but also by a sense of civic duty to inform the public and policy makers.

According to my analysis in the figure below, imposing an early (and necessarily temporary) lockdown would simply delay the spread of the epidemic without affecting the ultimate toll.

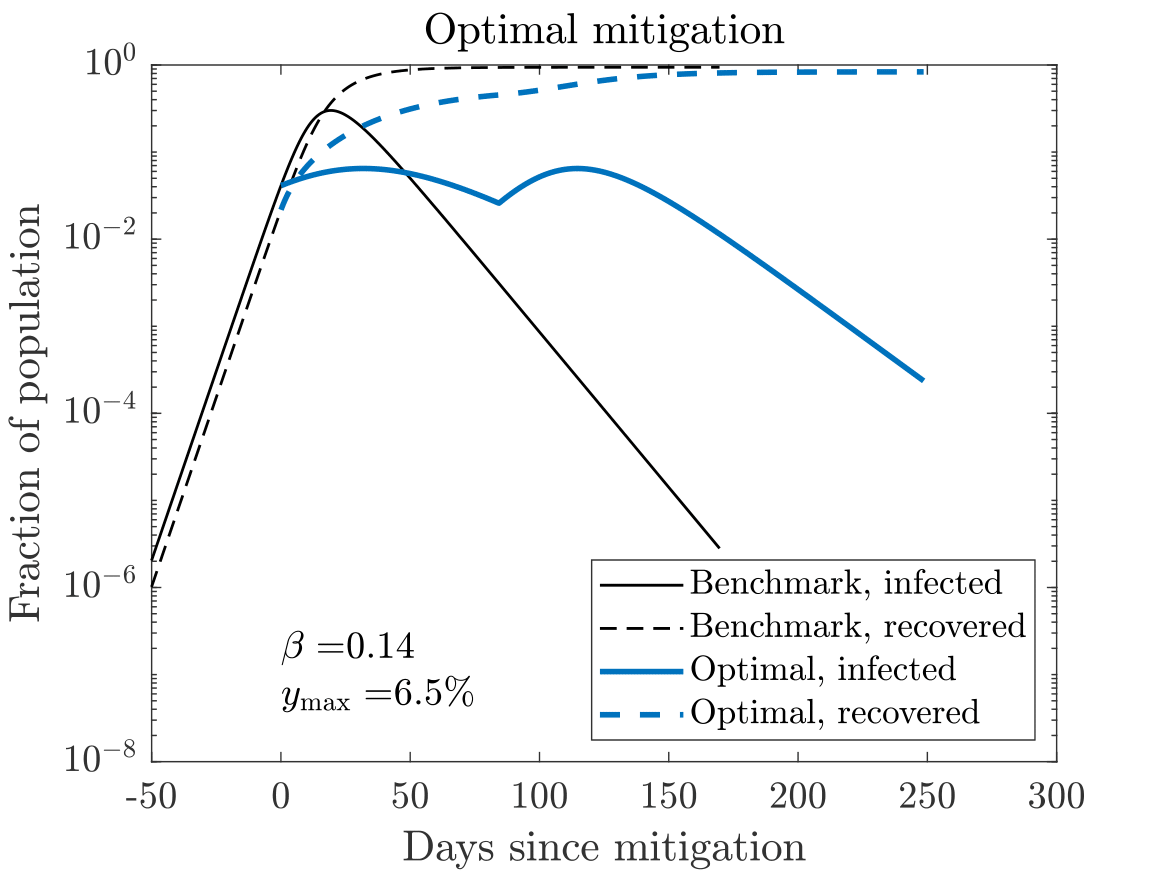

However, if the government delays intervention until about 1% of the population is infected, it would significantly reduce the total cumulative number of infections due to the build up of herd immunity, as the following figure shows.

The analysis was of course not perfect, but because I thought the problem was urgent, I submitted this paper to AER: Insights on March 26, 2020. I presented the paper at the UCSD Econometrics seminar on March 31, 2020, and the paper was included in the first issue of the working paper series Covid Economics. It was also featured in the April 2020 VoxEU and May 2020 Fortune articles. This paper is by far my most cited paper. Unfortunately, AER: Insights rejected my paper in May 2020, by which time so many things have changed and there was so much competition, so I gave up the project.

After this experience, I started to question the relevance of traditional economics research. I felt that the long review process at typical economics journals prevents researchers from working on pressing issues. Of course, one could write a sophisticated paper after the pandemic is long gone (instead of writing a preliminary paper in a few weeks), but what is the benefit to the society? I also felt that most COVID papers written by economists encouraged lockdown and sided with increased government control, perhaps because researchers wanted to play the good guy. Later, I published a more sophisticated paper in JET.

Published:

Published:

Published:

After my 2022 ECMA paper got accepted in January 2022, I got burnt out. I stopped doing research and spent most of my time playing tennis. I became a captain of a USTA 7.0 mixed doubles team (I had just become 4.0), and my wife and I recruited strong players, organized practices, and advanced to sectionals twice. In one of the Southern California sectionals, we narrowly lost in the semifinal.

My coauthor Jim Rauch was the recruitment chair when I got hired at UCSD in 2013. He was also the department chair from 2013 to 2016, so I had a lot of interaction with him. When we chatted in June 2022, he mentioned he was interested in a project to animate the contraction mapping theorem to help build intuition. We knew it had zero career benefit but it sounded fun, so I wrote up some pedagogical material and Matlab codes and Jim made the video.

We tried to publish this in journals on economic education but we got desk-rejected each time and the paper became dormant. Later, I was asked to review a paper at Qeios. Because I had never heard of that journal, I thought it was a predatory journal, but upon inspection its business model seemed interesting: they publish anything, but reviews are open and (to prevent abuse) not anonymous. So we posted our paper there, and we are happy that our paper and video have been well received.

Published:

In May 2023, I read something about Ergodicity Economics, and I thought it was a completely nonsense pseudoscience promoted by failed self-proclaimed physicists. Although it had zero career benefit, to contribute to the public good to prevent the spread of pseudoscience, I spent a few days writing this critique. The paper got desk-rejected from Physical Review Letters, Physical Review E, and Chaos and became dormant. After my pleasant experience at Qeios, I published the paper there.

Published:

I taught math camp at the UCSD economics PhD program from 2015 to 2023. A publisher noticed that I have been posting my lecture notes at my website and solicited its publication as a book. I completely rewrote my notes from 2023 to 2024. I think this is the best textbook on “Mathematics for Economics” out there.

Published:

This is a rejoinder to “Toward Bubble Clarity” published at Econ Journal Watch. See here for the history.

Published in Economic Theory, 2010

(Theory) Generalize Foley’s (1994) statistical equilibrium model when offer sets are endogenous; my master thesis at U of Tokyo; further generalized in Toda (2015).

Published in American Mathematical Monthly, 2011

(Mathematics) Simple proof of reverse monotonicity of the inverse of positive definite matrices based on convex conjugate functions.

Published in Physical Review E, 2011

(Power law, Empirical) A certain mean-reverting income process generates a stationary double Pareto distribution; an abridged version of my third-year empirical paper at Yale.

Published in International Journal of Psychiatry in Medicine, 2012

(Medicine, Empirical) The media coverage during the 2008 outbreak of hydrogen sulfide suicides in Japan caused more suicides.

Published in Journal of Economic Behavior and Organization, 2012

(Power law, Empirical) A certain mean-reverting income process generates a stationary double Pareto distribution; my third-year empirical paper at Yale.

Published in Economics Letters, 2013

(Numerical method) Simple maximum entropy method to discretize probability distributions.

Published in International Journal of Emergency Medicine, 2013

(Medicine, Empirical) You need to practice at least 30 times to intubate a patient consistently.

Published in International Journal of Geometry, 2014

(Mathematics) High-dimensional generalization of the fact that the sum of the reciprocals of the radii of escribed circles of a triangle equals the reciprocal of the radius of the inscribed circle; obtained those results in 1998 when I was freshman.

Published in Journal of Economic Theory, 2014

(Power law, Theory) Class of tractable dynamic general equilibrium models that generates power law in size distributions; one of my dissertation chapters at Yale.

Published in Economic Theory, 2015

(Theory) Walrasian equilibrium is a special limiting case of statistical equilibrium; extension of Toda (2010).

Published in SIAM Journal on Numerical Analysis, 2015

(Numerical method, Mathematics) Convergence and error analysis of maximum entropy discretization of Tanaka & Toda (2013).

Published in Journal of Political Economy, 2015

👍(Power law, Econometrics, Empirical) Power law in cross-sectional household consumption data causes spurious inference.

Published in Review of Economic Dynamics, 2015

(Theory, Macro, Finance) Asset pricing and optimal taxation in a class of tractable dynamic general equilibrium models; formerly a section of Toda (2014).

Published in Economic Theory Bulletin, 2017

(Theory) Many general examples of multiple equilibria in Edgeworth box economies.

Published in Quantitative Economics, 2017

After working on the maximum entropy discretization method in Tanaka & Toda (2013, 2015), in 2014 I wanted to apply the method for discretizing Markov processes. Because I had neither sufficient programming skills nor knowledge of potential applications, I asked my colleague Johannes Wieland if he knew a good graduate student to work with, and he referred me to Leland. At that time, Leland was working on the estimation of nonlinear state space models using discretization (which later became his job market paper), so our interests aligned. Leland played an instrumental role for this project such as suggesting discretizing the conditional distributions, coding, and finding interesting applications. We owe Craig Burnside for suggesting using a closed-form asset pricing model to evaluate solution accuracy, and Jim Hamilton for suggesting avoiding simulations entirely.

We initially submitted this paper to Econometrica. We had two positive and two negataive reports, and one of the negative one complained about the possibility of matching higher order moments, which we pointed out in a footnote but did not implement out of laziness. I regret that maybe if we did it from the beginning, we might have been able to publish this paper at Econometrica. When we sent the paper to QE, we exercised the option to transfer Econometrica reports, and the review process was painless.

I believe the discretization method in this paper is still the best in the literature and has been applied in many papers by other researchers. Please see my discretization page for up-to-date files.

Published in Journal of Applied Econometrics, 2017

(Power law, Econometrics, Finance) Monte Carlo study of spurious inference caused by power law; formerly a section of Toda & Walsh (2015).

Published in Macroeconomic Dynamics, 2017

(Power law, Empirical) Cross-sectional household consumption is well-approximated by double Pareto-lognormal distribution; formerly a section of Toda & Walsh (2015).

Published in Journal of Mathematical Economics, 2017

(Theory, Macro) In perpetual youth models, introduction of government transfer crowds out annuity market and increases growth.

Published in Journal of Economic Dynamics and Control, 2017

(Theory, Macro) Closed-form solution to a Huggett (1993) economy with non-Gaussian VAR(1) dynamics and general examples of multiple stationary equilibria.

Published in Journal of Financial Economics, 2019

(Finance, Theory) With collateral constraints, financial integration may hurt the less constrained country.

Published in Journal of Monetary Economics, 2019

(Power law, Theory, Macro) Formal proof that the Krusell & Smith (1998) random discount factor trick generates power law tails; Pareto exponent is sensitive to the calibration of discount factor process.

Published in Journal of Economic Theory, 2019

👍(Power law, Theory, Macro) Prove the impossibility for the canonical Bewley-Huggett-Aiyagari model to generate heavier-tailed wealth than income.

Published in Econ Journal Watch, 2019

(Empirical) Publications (Top 5/Non-top 5) and job rank explains over 80% of variations in salaries among economics professors in the UC system; no evidence of gender gap

Published in Journal of Economic Theory, 2020

(Power law, Theory) Establish existence and uniqueness of a solution to a general income fluctuation problem; characterize tail behavior of stationary wealth distribution.

Published in Review of Financial Studies, 2020

👍(Finance, Theory, Empirical) In general equilibrium model with heterogeneous risk aversion and/or beliefs, the wealth distribution predicts excess stock returns, which we confirm in data using estate tax rate change as instrument.

Published in Empirical Economics, 2020

(Power law, Empirical) The majority of data sets analyzed by Gibrat and claimed to be lognormal are actually closer to Pareto-type distributions.

Published in Physica D: Nonlinear Phenomena, 2020

👍(Power law, Empirical) Size distribution of COVID-19 cases across US counties as of March 2020 obeys the power law; empirical Pareto exponent is consistent with the estimated growth rate and age distributions.

Published in Journal of Applied Econometrics, 2021

(Power law, Econometrics) Efficient estimation of Pareto exponents when only certain top income shares are observable.

Published in Journal of Economic Interaction and Coordination, 2021

(Network) Simulation study of the evolution of an epidemic disease on social networks; the effectiveness of social distancing greatly depends on network structure.

Published in Journal of Economic Theory, 2021

👍(Theory, Macro) Prove asymptotic linearity of policy functions when preferences are homothetic; show that asymptotic marginal propensities to consume can be zero, implying a large saving rate of the rich.

Published in Computational Economics, 2021

(Numerical method) Automatic discretization method of nonparametric distributions using Gaussian quadrature.

Published in Journal of Mathematical Economics, 2021

👍(Theory) That HARA utility implies concave consumption functions is well-known, but the converse is also true.

Published in Operations Research Letters, 2021

(Mathematics) Show the usefulness of Perov’s contraction principle (which is a generalization of Banach’s contraction principle) for solving certain dynamic programming problems.

Published in Journal of Mathematical Economics, 2022

(Theory, Numerical method) Prove asymptotic linearity of policy functions when marginal utility is regularly varying; follow-up of Ma & Toda (2021).

Published in Journal of Mathematical Economics, 2022

(Theory) Simple operation that often transforms an unbounded dynamic programming problem into a bounded one.

Published in Econometrica, 2022

To obtain the double power law result in my 2014 JET paper, I assumed some conditional independence (which rules out persistent heterogeneity) and took the continuous-time limit, which was not entirely satisfactory. In those days, all power law results in economics relied on the IID assumption, which is clearly unrealistic. Around Footnote 13, Gabaix (1999) states

Published in Econometric Theory, 2022

This is a follow up paper of Beare & Toda (2022), where we characterize the tail behavior of Markov-modulated Lévy processes that are stopped at state-dependent Poisson rates. In 2018, Brendan gave the project to Won-Ki, who was his student. I joined Won-Ki’s dissertation committee to advise on this project, and we essentially translated the discrete-time results in Beare & Toda (2022) to continuous-time. The CARA-Huggett economy example in Section 4 was recycled from an earlier version of Beare & Toda (2022).

Published in Journal of Economic Theory, 2022

👍(Theory) Study a behavioral SIR model with imperfect testing and government enforcement and show that equilibrium action is approximately static efficient in the sense that the laissez faire equilibrium allocation is close to the optimal short-term lockdown policy, implying that short-term lockdown policies are redundant.

Published in Review of Income and Wealth, 2022

(Power law, Empirical) Estimate capital and labor income Pareto exponents across 475 country-year observations and document that capital income inequality is higher than labor income inequality (median Pareto exponents 1.46 and 3.35 respectively) and the two inequalities are uncorrelated, suggesting importance of distinguishing the two.

Published in Quantitative Economics, 2023

👍(Power law, Numerical method, Macro) Analytical framework designed to solve and analyze heterogeneous-agent models that endogenously generate fat-tailed wealth distributions.

Published in Theoretical Economics, 2023

(Theory) Robust comparative statics for the elasticity of intertemporal substitution; sign- and point-identification of EIS minus 1.

Published in Journal of Econometrics, 2024

(Econometrics) Just like what the title says, for example estimation of income distributions from tax returns data.

Published in Journal of Mathematical Economics, 2024

👍(Theory, Macro, Finance) Self-contained review of the theory of asset price bubbles.

Published in Economics Letters, 2024

I started to study models of bubble and money in late 2022 and learned the usefulness of the local stable manifold theorem. During my studies, I noticed that there is often hand-waving in applied works. For instance, Blanchard & Fishcer (1989, p. 268, Endnote 16) state

Care must be taken in using a phase diagram to analyze the dynamics of a difference equation system. […] Thus we must check in this case whether the system is indeed saddle point stable […]. This check is left to the reader.

Furthermore, during the review process of the bubble necessity paper, we learned about Scheinkman (1980)’s sufficient condition for local determinacy that involves the curvature of the utility function, which was a bit mysterious. So after resubmitting our paper to JPE at the end of December 2023, we started to work on a complete analysis of the local determinacy of equilibria in Tirole (1985)’s model. It turns out that Scheinkman’s sufficient condition does not generalize to production economies: there are robust examples with arbitrary utility functions in which the nonmonetary steady state is locally determinate or indeterminate. In contrast, the monetary steady state is locally determinate under fairly weak conditions.

Published in Journal of Mathematical Economics, 2024

The Journal of Mathematical Economics, which was founded in 1974, was running a 50th anniversary issue and Kieran (associate editor at JME) was invited to contribute a review article. As we have worked on equilibrium uniqueness, he invited me to write an article together.

Published in Economic Theory Bulletin, 2024

(Theory) Combine weighted supremum norm and Perov contraction theorem for solving unbounded dynamic programming problems.

Published in Journal of Political Economy, 2025

In the fall of 2022, Tomohiro Hirano, Ryo Jinnai, and I studied a model in which the interaction between idiosyncratic investment risk, leverage, and the presence of a dividend-paying asset in fixed supply affects asset prices. Tomohiro and Ryo had already worked on asset price bubbles including Hirano and Yanagawa (2017) and Guerron-Quintana, Hirano, and Jinnai (2023), whereas it was a new topic for me. This collaboration led to the working paper of Hirano, Jinnai, and Toda (2023) “Necessity of Rational Asset Price Bubbles in Two-Sector Growth Economies”, which we posted to arXiv in November 2022.

We submitted the paper to Econometrica in January 2023. It was rejected on May 5, 2023. We had three reports. The first report, written by an expert, was on the fence but found the example of nonexistence of fundamental equilibrium (Proposition 2.2) “extremely surprising” and stated that

[the] interesting contribution of the paper is … to show that there might be settings where equilibria without bubbles do not exist.

The second report was likely written by a quantitative macroeconomist, declined to evaluate the theoretical contributions, and recommended rejection, while acknowledging that

What’s more of a surprise, is that under some conditions, we necessarily go to \(R=G\).

The third report was written by an expert and provided many comments. One of them was

Miao and Wang (2018, AER) … also study models of bubbles attached to assets with positive dividends/rents

and another was

I am not convinced by one of the main result of the paper that an equilibrium with rational asset price bubbles exists but equilibria with asset prices equal to fundamental values do not,

though this referee did not point out any specific mathematical error.

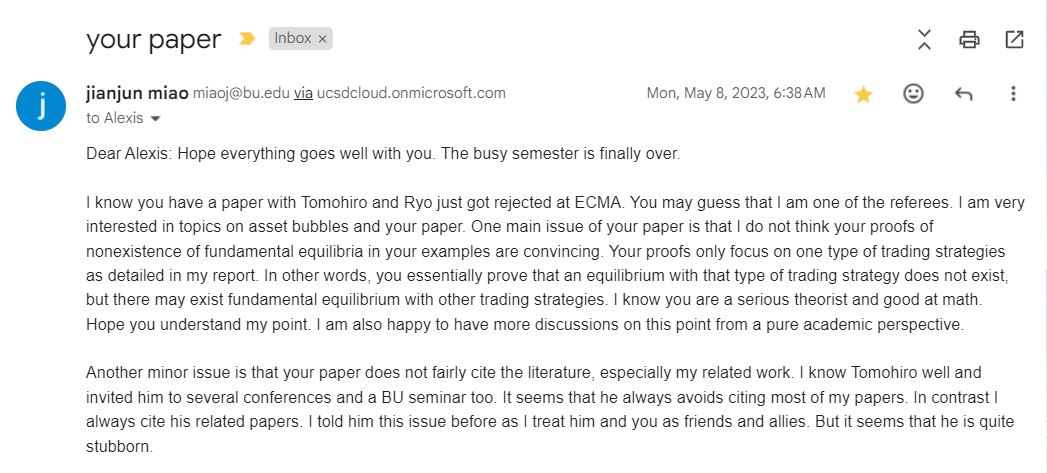

Three days later, on May 8, 2023, Jianjun Miao sent an email to me, in which he disclosed that he was the third referee at Econometrica.

In case it is difficult to read, I quote it here.

I know you have a paper with Tomohiro and Ryo just got rejected at ECMA. You may guess that I am one of the referees. I am very interested in topics on asset bubbles and your paper. One main issue of your paper is that I do not think your proofs of nonexistence of fundamental equilibria in your examples are convincing. Your proofs only focus on one type of trading strategies as detailed in my report. In other words, you essentially prove that an equilibrium with that type of trading strategy does not exist, but there may exist fundamental equilibrium with other trading strategies. I know you are a serious theorist and good at math. Hope you understand my point. I am also happy to have more discussions on this point from a pure academic perspective.

Another minor issue is that your paper does not fairly cite the literature, especially my related work. I know Tomohiro well and invited him to several conferences and a BU seminar too. It seems that he always avoids citing most of my papers. In contrast I always cite his related papers. I told him this issue before as I treat him and you as friends and allies. But it seems that he is quite stubborn.

The part “other trading strategies” is a bit strange, as our example employed a two-period overlapping generations model in which the unique portfolio choice in equilibrium is that the old sell the entire asset and the young buy the entire asset (which is necessarily true by market clearing). After this exchange, I offered to explain the proof in a Zoom meeting with Miao, but he insisted that a fundamental equilibrium (an equilibrium with \(P=V\)) always exists and was not willing to listen.

At this point, Tomohiro and I were not yet aware of the issues with Miao and Wang (2018) discussed in our clarification paper (subsequently published at Econ Journal Watch) or this post, but we were encouraged by the first referee’s reaction of “extremely surprising”, so we decided to write a new paper to establish the robustness of the nonexistence of fundamental equilibria. We worked intensively for a week and posted a new working paper “Bubble Necessity Theorem” to arXiv on May 14.

After polishing, we submitted this paper to Econometrica on June 21, 2023, this time attaching a cover letter detailing the conflict of interest with Miao. This paper was desk-rejected without any feedback from the editor: you can see the decision letter here.

Being worried if the cover letter was the cause of rejection, we then submitted the paper to Journal of Political Economy without a cover letter. Fortunately, we received a revision request on September 5, 2023 with three positive reports. After several revisions, the paper was accepted on April 23, 2024 and was published in 2025.

We will keep fighting for scientific integrity.

Published in International Journal of Game Theory, 2025

In the academic year 2021, Longjian (then undergraduate student at Peking University) visited UCSD for an exchange program. He asked me if he could take the first year PhD microeconomics. Normally I don’t allow undergraduate students to take PhD classes, because almost all precedents failed to keep up with the coursework. However, looking at Longjian’s CV and academic transcript, I realized that he had taken many advanced math courses and excelled in all of them, so I took the chance and allowed him to take the course. He ended up in the top quarter of the PhD cohort, so his performance was impressive.

During the course, Longjian regularly came to my office hours and discussed his research interest. He explained to me the secretary problem, that early applicants have no incentive to show up for interviews because they get rejected for sure, and so on. He worked on an example with two or three agents in which the administrator needs to incentivize them to show up for interviews. I told him to use dynamic programming to solve the general case with \(N\) agents. He did, and he also proved the optimality of the full learning equilibrium. Later, I added a result on the asymptotic behavior of success probability, and we wrote this paper together.

Although it took us two years to get the paper published (we got rejected from Games and Economic Behavior, Operations Research, and Economic Theory), I am happy that we eventually published it in a decent journal.

Published in Econ Journal Watch, 2025

In the fall of 2022, Tomohiro Hirano, Ryo Jinnai, and I studied a model in which the interaction between idiosyncratic investment risk, leverage, and the presence of a dividend-paying asset in fixed supply affects asset prices. This collaboration led to the working paper of Hirano, Jinnai, and Toda (2023) “Necessity of Rational Asset Price Bubbles in Two-Sector Growth Economies”, which we posted to arXiv in November 2022.

We submitted the paper to Econometrica in January 2023. It was rejected on May 5, 2023. One report was written by an expert and provided many comments. One of them was

Miao and Wang (2018, AER) … also study models of bubbles attached to assets with positive dividends/rents

and another was

I am not convinced by one of the main result of the paper that an equilibrium with rational asset price bubbles exists but equilibria with asset prices equal to fundamental values do not,

though this referee did not point out any specific mathematical error.

Three days later, on May 8, 2023, Jianjun Miao sent an email to me, in which he disclosed that he was the third referee at Econometrica.

In case it is difficult to read, I quote it here.

I know you have a paper with Tomohiro and Ryo just got rejected at ECMA. You may guess that I am one of the referees. I am very interested in topics on asset bubbles and your paper. One main issue of your paper is that I do not think your proofs of nonexistence of fundamental equilibria in your examples are convincing. Your proofs only focus on one type of trading strategies as detailed in my report. In other words, you essentially prove that an equilibrium with that type of trading strategy does not exist, but there may exist fundamental equilibrium with other trading strategies. I know you are a serious theorist and good at math. Hope you understand my point. I am also happy to have more discussions on this point from a pure academic perspective.

Another minor issue is that your paper does not fairly cite the literature, especially my related work. I know Tomohiro well and invited him to several conferences and a BU seminar too. It seems that he always avoids citing most of my papers. In contrast I always cite his related papers. I told him this issue before as I treat him and you as friends and allies. But it seems that he is quite stubborn.

The part “other trading strategies” is a bit strange, as our example employed a two-period overlapping generations model in which the unique portfolio choice in equilibrium is that the old sell the entire asset and the young buy the entire asset (which is necessarily true by market clearing). Anyway, we subsequently expanded this example as a new paper, which got published at Journal of Political Economy (after getting desk-rejected from Econometrica).

While working on the JPE paper, we learned about the Bubble Characterization Lemma of Montrucchio (2004), which states that a rational bubble exists if and only if the infinite sequence of dividend yields (dividend divided by the price) is summable. Using this result, it became obvious that the model in the 2018 AER paper of Miao and Wang does not generate rational bubbles (contrary to their claim in their abstract) because their model admits a steady state with positive dividends and prices. Thus, to clarify the confusion in the literature, when we published our 2024 JME review article, we wrote in Footnote 13 that the Miao-Wang model is different from the so-called rational bubble models.

Subsequently, we wrote several papers on asset price bubbles, and we received multiple (negative) anonymous referee reports claiming that we do not fairly cite the literature, that papers by Miao and Wang also study models of bubbles attached to assets with positive dividends, or that our research is just a derivative of the previous literature with a small twist. However, the Miao-Wang model is completely different from rational bubble models, so we felt the need to defend ourselves from biased referees and to clarify the confusion in the literature. This is why we wrote our paper initially titled “Rational Bubbles: A Clarification” and posted to arXiv in July 2024. After posting the working paper, we received supports from experts such as

I have in fact had doubts about Jianjun Miao’s claims that rational bubbles are easy to generate in production economies. Specifically, in one of his papers he conveniently omitted checking one of the key equilibrium conditions. I cannot remember now whether it was the 2018 paper or some other paper. It has always been surprising to me that they chose not to provide an explanation of how these models get away from Santos-Woodford powerful no-bubble theorem.

You have my full support. It is very important to find out when rational bubbles do exist, but not by contradicting the fundamental results.

and

We had a long discussion on Miao’s paper, we also had notes, but I could not find them anymore. I remember that paper was very confusing. In addition, we had noticed some misalignment between different uses of the concept of bubble, because there is some disagreement on the idea of fundamental, or intrinsic, value.

We submitted this paper to American Economic Review as a comment to Miao and Wang (2018). AER rejected our comment and sent us Miao and Wang’s referee report. (This report contains many false statements. You can read our response here.) There were other anonymous reports (who all recommended rejection), but only one of them seem to be written by an expert. Therefore, we decided to submit the paper to Econ Journal Watch.

After our paper went through peer review and got accepted at EJW, Miao wrote me an email:

Dear Alexis:

I just found that your comment paper Rational Bubbles: A Clarification is just published by Econ Journal Watch.

Your paper was rejected by all referees at AER. I think their reports are very similar and believe your comments on my AER paper with Pengfei do not make much sense. I do not understand you still insist on publishing it in some unknown journal that even does not ask us for a response. I do not understand what your point is. As both Pengfei and I have made it clear, we are in a small circle working on the area of bubbles. We treat you as a friend and ally. We should be friendly to each other to make this area more prosperous. We do not want to enter a bad equilibrium.

EJW always invites the commented-on authors to respond, so I am looking forward to Miao’s response. To us, what Miao, Wang, and the AER are doing are difficult to understand. If a model has been understood as a rational bubble model, but in fact it was not, it seems worth publishing a correction or a clarification. Instead, some editors and reviewers in the profession seem to try to silence us. In the above email, Miao wrote “We should be friendly to each other to make this area more prosperous. We do not want to enter a bad equilibrium.” Is he suggesting that we should rubber-stamp a paper of a “friend”? Is he suggesting that he will retaliate if we don’t do so, which is a “bad equilibrium”? We are not going to succumb to such intimidations. We are going to fight for truth and science.

Published in Proceedings of the National Academy of Sciences, 2025

This is my fourth paper on rational bubbles. The first paper is “Necessity of Rational Asset Price Bubbles in Two-Sector Growth Economies”, which we posted on arXiv in December 2022. (The paper is still unpublished and its title has changed a few times, though we expanded the example in Section 2.2.1 as an independent paper and published at JPE.) The second paper is “Equilibrium Selection in Pure Bubble Models by Dividend Injection”, which we posted on arXiv in March 2023 and still unpublished. The third paper is “Housing Bubbles with Phase Transition”, which we also posted on arXiv in March 2023 and still unpublished.

When we initially discovered the necessity of bubbles (i.e., bubbles inevitably emerge under some conditions), the example was based on an endowment economy with growth and constant dividends. After discovering this example, I became interested in applications. Because land and housing are typical assets on which bubbles often arise (at least in the casual sense), I worked on several models that could generate endogenous dividends. After some trial and error, I realized that the elasticity of substitution (either in the utility function of the production function) plays an important role: once we remove the knife-edge restriction of elasticity being exactly equal to 1 (Cobb-Douglas), the economy and dividends grow at different rates (unbalanced growth), which generates bubbles under a low interest rate condition. This paper emerged from this idea: empirical evidence suggests that the elasticity of substitution between land and non-land factors exceeds 1, so when the economy grows, land rents do not grow as fast and generates a land bubble.

We submitted the paper to American Economic Review in July 2023. We got rejected in October 2023 with one positive report, one on the fence, and one negative. Around that time, we got an R&R from JPE for the necessity paper, so we thought it more advantageous to wait until JPE accepts the paper to have a better reputation. Therefore, we let the paper be dormant for a year, and I used this paper as my job market paper when I was on the market in Fall 2023. After JPE accepted our paper, we revised the unbalanced growth paper. Because some AER referees asked for more empirical work, which we don’t have any expertise, we shortened the paper and submitted to American Economic review: Insights in August 2024. We got rejected in November 2024 with just one, one-page report.

At that point we had too many pending projects, and we had no intention of bloating the paper with empirical work or extensions, so we decided to submit the paper to Proceedings of the National Academy of Sciences in November 2024, which is a top science journal. (And being a science journal, papers are much more concise than those in economics journals. An added benefit of PNAS is that you can suggest 6 potential reviewers and 3 you would like to exclude from reviewing, so we can suggest true experts and avoid people with conflicts of interest.) We received a minor R&R with two positive reports in December 2024 and got accepted shortly after we resubmitted in February 2025. I have been submitting hundreds of papers to different journals, but science journals provide far better experience than economics journals.

Published in Cliometrica, 2025

I owe a great deal to coauthor Vincent Geloso for this paper. Vincent has written a series of papers that improve the top income share estimates. In 2023 he found my paper on nonparametric density estimation from tabulated summary data and suggested that we apply the method to estimate top income shares from tax returns data. At that time, the literature used Piketty’s Pareto interpolation method, which was ad hoc.

Published in Economic Inquiry, 2025

In this paper, we find that by replacing the labor income tax by a value-added tax and maintaining a capital income tax, we can improve welfare by a staggering 7%.

It took a long time for this paper to get shaped and published. In 2017, Brendan and I wrote a paper that characterizes the Pareto exponent of the stationary distribution of a Markov multiplicative process with reset. Section 4 of that paper contains an application to the wealth distribution of a Huggett model with constant absolute risk aversion (CARA) utility. We submitted this paper to Econometrica and received a “reject and resubmit”. Reviewers complained that the application generates a wealth distribution with exponential tails, not Pareto tails. Hence, in the revised version, we changed the model to a version of the Angeletos model. When we received a “revise and resubmit” from Econometrica, the editor asked us to cut this application to shorten the paper.

So, the paper became dormant for a while. As I like to recycle materials, I rewrote the paper with a quantitative focus on optimal taxation. Initially, there was just capital and labor income taxes, but when Brendan presented the paper at Duke, John Coleman suggested that we should also include consumption tax (value-added tax). This was an extremely helpful suggestion because the welfare implications changed completely, from a modest (around 1%) increase in consumption equivalent to a staggering 6.6%.

After revising the paper, it was a long shot but we submitted the paper to Journal of Political Economy, and not surprisingly, got rejected. We then submitted the paper to Journal of Public Economics and received a “revise and resubmit”. However, the reviewers asked too many things that we thought were infeasible. Brendan discovered that Economic Inquiry allows the option of “no revision policy” (meaning the paper gets accepted as is or rejected). As we were not willing to spend effort on additional quantitative work, we withdrew the paper from JPubE and submitted it to EI. The review process took only two months and the paper got accepted as is, so I am very happy.

Let me also point out that EI is serious about replicability (so preparing replication files requires effort), which I think is a good thing.

Published in Economics Letters, 2025

In any rational bubble model with a dividend-paying asset, the dividend yield (dividend to price ratio) must converge to zero in the long run (see, for instance, Lemma 1 of my JPE paper). Some people have a strong belief that the dividend yield should be stationary and reject the idea of rational bubbles on this basis.

I presented my housing paper at Princeton on September 30, 2024. The audience was very smart, and the paper was well received. Regarding the dividend yield (rent yield in the case of housing), Nobuhiro Kiyotaki suggested that if we introduce the construction of housing, we need to separate the rent accruing to the housing structure and that to land. Consequently, it could be the case that there is a land bubble (the ratio between the pure land rent and land price converges to zero) but the housing rent to price ratio appears to be stationary. This was a very smart insight, and after going back to my hotel room, I wrote up a simple version of the model along these lines.

Subsequently, although Tomohiro Hirano and I have been successful in publishing a few papers on rational bubbles including Journal of Political Economy and Proceedings of the National Academy of Sciences, for other papers we keep getting pushbacks from non-experts, dogmatic reviewers, or those with conflicts of interest. Being fed up with this situation, I decided to publish my note to shut down the claim that “rent yield should be stationary”.

I submitted my paper to Economics Letters on October 25, 2025. Upon checking its status, I saw that it was reviewed within a few days, and I received a formal letter of acceptance on October 29, 2025. Although acceptance as is has happened to me before (once at Journal of Economic Theory, once at Journal of Mathematical Economics (before I became a coeditor, of course), and once at Economic Inquiry), getting a paper accepted in 4 days is my fastest ever. I applaud the editorial board of Economics Letters for upholding science and disseminating scientific knowledge without delay (unlike some club journals).

Published in Econometrica, 2026

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Published:

Download here

Undergraduate, UCSD, 2015

This course covers some topics in operations research, such as convex analysis, nonlinear programming, and dynamic programming. I do not currently teach this course.

Graduate, UCSD, 2016

This course trains third year Ph.D. students to conduct research, write papers, and make presentations.

Graduate, UCSD, 2017

This course covers topics in finance theory. I do not currently teach this course.

Graduate, UCSD, 2023

This course covers mathematical topics that are essential for economics, very quickly but rigorously.

Undergraduate/Graduate, UCSD, 2023

This course covers the classical Arrow-Debreu theory of general equilibrium. The undergraduate course (Econ 113) meets 3 hours per week for 10 weeks and covers about 2/3 of the lecure notes. The graduate course (Econ 200A) meets 3 hours per week for 5 weeks and covers the entire lecture notes plus additional topics on mathematical economics.

Undergraduate, UCSD, 2024

This course covers some institutional details on the financial markets, bond pricing (including duration analysis), optimal portfolio problem, mutual fund theorem, Capital Asset Pricing Model, and option pricing (including bounds on option prices, suboptimality of early exercise of American call options, put-call parity, and binomial option pricing).

Undergraduate, Emory, 2025

This course studies personal finance, some institutional details on the financial markets, bond pricing (including duration analysis), optimal portfolio problem, mutual fund theorem, Capital Asset Pricing Model, and option pricing (including bounds on option prices, suboptimality of early exercise of American call options, put-call parity, and binomial option pricing). The course requires good analytical skills (basic calculus and probability/statistics). To solve numerical examples, we will learn programming in Matlab, although no prior knowledge is necessary.

Published:

Published:

Published:

Published:

Published: